- Meyka AI's Newsletter

- Posts

- CPI Data, Stock Market Volatility, and US-Iran Ceasefire Talks Drive Global Market Sentiment

CPI Data, Stock Market Volatility, and US-Iran Ceasefire Talks Drive Global Market Sentiment

This week's edition covers:

What is the S&P 500 record actually telling you?

One tanker crossing a closed strait, and what it means

Why did BofA just push rate cuts to 2027?

The bias that has burned investors four times since January

Let's get into it.

Market Mood Snapshot

Is This Rally For Real?

Markets are at record highs. But the mood does not feel like a celebration.

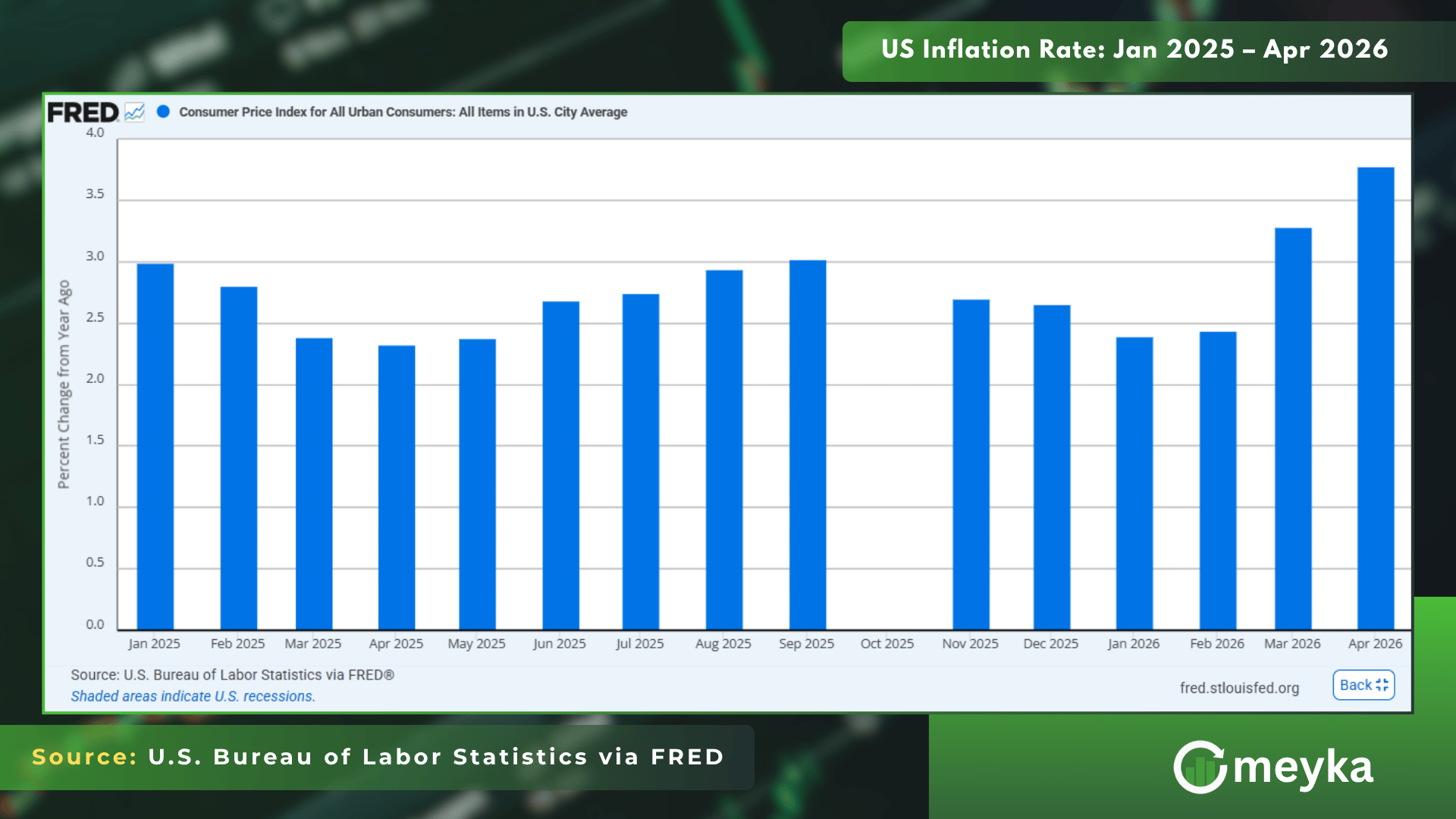

The S&P 500 closed at 7,412 on Monday. The Nasdaq touched a fresh all-time high at 26,274 on Monday. By Tuesday morning, after the CPI landed, it was already falling. But underneath, investors are nervous.

Oil is swinging daily. A ceasefire is ‘on life support.’ And this morning, the answer arrived. April CPI came in at 3.8% year over year, the highest since May 2023. Stock futures turned negative. Treasury yields climbed. The rally that was looking over its shoulder just found what it was looking for.

Meyka AI: NASDAQ 100 (^NDX) Index Overview, May 2026

Two-Minute Weekly Brief

Here is what happened this week, fast:

Inflation jumped hard in March. The CPI rose 3.3% year over year, the highest since May 2024. Consumer prices surged 0.9% in a single month, the biggest monthly jump since June 2022. The culprit: gasoline up 18.9%, fuel oil up 44.2%. The Iran war drove this.

April CPI confirmed the concern. The BLS reported prices rose 3.8% year over year in April, the highest since May 2023, beating the Dow Jones consensus of 3.7%. Core CPI, which excludes food and energy, came in at 2.8% annually, its highest monthly rate since January 2025. Shelter costs rose 0.6%, and real average hourly wages fell 0.3% annually.

The US-Iran ceasefire is barely alive. Trump called it ‘on life support’ on Monday. Iran's latest counter-proposal was rejected as ‘TOTALLY UNACCEPTABLE.’ The Strait of Hormuz, a waterway carrying roughly 20% of global seaborne oil, has been largely blocked since late February.

The Fed is stuck. BofA now expects zero rate cuts in 2026, pushing its forecast to July 2027. The Fed held rates at 3.50-3.75% at its April 29 meeting in an unusually divided 8-to-4 vote, the closest internal split since 1992. CME FedWatch shows roughly 70% probability of another hold at the June meeting.

Money Minute 💡

One-Minute Finance Lesson

Oil price shocks often act like a hidden tax on the economy. When oil rises, transport and production costs increase, and prices slowly spread through goods and services. This is called cost-push inflation. It matters because it can delay interest rate cuts even when growth is slowing.

One takeaway: Oil does not just move energy markets; it quietly reshapes monetary policy.

Noise vs Signal

Noise: “Markets hit all-time highs, everything is fine.”

It sounds reassuring. It is not the full picture. The S&P and Nasdaq did touch record levels this week but Charles Schwab analysts made a critical point: the rally after the ceasefire announcement in early April was driven largely by investors unwinding their hedges and closing short positions, not by any genuine improvement in conditions.

When traders who were betting on bad news close those bets, prices go up. That is not optimism. That is positioning.

Signal: The Fed is more constrained than at any point in recent years.

This is what actually matters. Core CPI came in at 2.8% in April, above the 2.7% expected. Inflation is no longer just an energy story. Outgoing Fed Chair Powell said energy shocks tend to be temporary. But he also acknowledged this shock follows years of already-elevated prices.

The Fed cannot cut without risking inflation expectations coming unanchored. It cannot rise without risking economic damage.

What Most Missed:

The Fed's internal fracture

The April 29 FOMC meeting ended in an 8 to 4 vote. That is the most divided the Fed has been since 1992. One governor voted to cut. Three others objected to the language in the post-meeting statement. This kind of public disagreement is rare.

BofA said it plainly in a note this week: ‘Core inflation is too high, and moving up.’ Deutsche Bank added that trend inflation has ‘not shown clear signs of dipping below 3%.’ When the institution setting interest rate policy cannot agree internally on direction, the uncertainty downstream for bonds, mortgages, and equities multiplies.

The Hormuz problem has no quick fix

Even if a peace deal is signed tomorrow, the Strait of Hormuz will not normalize quickly. The Joint Chiefs confirmed 22,500 mariners are trapped on more than 1,550 vessels. Kpler estimates 170 million barrels of oil are sitting aboard 166 stranded tankers, and clearing them once the strait reopens could take up to three months.

Schwab analysts noted this clearly: energy prices could stay elevated well after any formal end to hostilities. That fact alone keeps inflation forecasts uncomfortably high through the second half of 2026.

One Chart, One Story:

Picture a line that runs flat across most of 2025, dips to 2.4% in January and February 2026, and then in March jumps sharply to 3.3%. That is the US headline inflation chart for the past 14 months.

The story it tells is straightforward. Inflation was finally cooling. The Fed's work appeared to be showing results. Then the US-Iran conflict began in late February, and one geopolitical shock reversed much of that progress in a single month.

April confirmed it was not a one-month spike. CPI came in at 3.8% year over year, the highest since May 2023, up half a percentage point from March in a single month. Energy drove over 40% of the gain, with gasoline up 28.4% annually. But the more important detail is what else moved. Shelter rose 0.6%. Airline fares climbed 2.8% in one month. Food at home posted its biggest monthly gain since August 2022. Core CPI, which strips out energy entirely, still came in at 2.8%. The war's cost is no longer staying inside the energy bill.

If the Hormuz situation stabilizes, this chart could reverse. If it does not, the next few months on that line will tell investors more about the direction of this economy than almost anything else.

Opportunity Lens

The Strait Is Closed. So, Where Do You Look?

When markets are unstable, the temptation is to either exit quickly or stop paying attention. Neither tends to serve investors well. What volatility actually does is create differentiation.

Consider two scenarios from here.

‘If the Strait of Hormuz gradually reopens, global trade normalizes, shipping companies and supply chain stocks benefit, and energy price pressure eases.’

‘If conflict resumes, upstream oil producers that extract crude and benefit directly from high prices continue to see strong earnings in a $100+ oil environment.’

Both outcomes have identifiable implications. The more durable long-term theme may be energy security itself: the rerouting of supply chains, the buildout of alternative energy routes, and the reshoring of critical infrastructure. That trend was already building before February 2026. The war has made it a national policy priority across Europe, Asia, and Gulf states.

Investors who think in years, not weeks, may find that shift more meaningful than any short-term trade.

Investor Mind Gym

This week's bias: Recency Bias

Recency bias is the tendency to assume that whatever just happened is likely to keep happening. After a bad month, investors expect more bad months. After a strong rally, they assume it continues. It is one of the most common and costly patterns in market behavior.

Meyka AI: Dow Jones Industrial Average (^DJI) Index Overview, May 2026

This week is a live case study. When the ceasefire was announced in early April, the Dow surged over 1,000 points in a single session. Many investors interpreted that as a resolution. It was not. The ceasefire began unraveling almost immediately.

By May, Trump was calling it ‘unbelievably weak.’ Investors who saw the April rally and assumed the crisis was over had fallen into recency bias. The real signal one that required patience to read was that structural problems like the Hormuz blockade, Iran's nuclear red lines, and a stalled diplomatic process do not resolve in days.

Catching this bias does not mean expecting the worst. It means asking one honest question before acting: Is this new information, or am I just reacting to the last thing I saw?

Ask Meyka: So What Do You Do Now? 🧐

Here is the truth about this week. The data is complicated. The geopolitics are unresolved.

Today's CPI answered one question. At 3.8%, it confirmed that inflation is running at its fastest annual pace since May 2023. But it did not answer the more important ones: how long the Strait stays closed, and whether the Fed's patience has a ceiling.

What we do know is that the underlying economy is not broken. The inflation problem is largely external and traceable to one conflict. History shows that supply shocks, while painful, pass.

The investors who come out ahead are rarely the ones who predicted every turn. They are the ones who stayed clear on what they owned and why.

Disclaimer:

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.